InsurTechs often point to the vastness of the opportunity within a $250bn marketplace and say there is a place for everyone. However, in our prior note ("Unsurtech and the temple of Underwriting Doom") we noted that from an InsurTech's vantage point, they (falsely) believe a newco can penetrate the market because of: (a) commoditized product; (b) low cost of tech and software; (c) data analytics; and (d) simple distribution channel.

A line is often drawn from FinTech to InsurTech and how several offerings disrupted the legacy sectors, including financial services, transportation, real estate etc. What is less talked about is how insurance is a tough place to make money.

You are pricing a product without knowing the actual cost of goods sold. More often than not, there is a disconnect between the two. For example, we noted previously that P&C insurance is a high-single-digit return business barely exceeding the cost of capital at the best of times.

It would be easy to say we told you so based on our past writings, but we are sure that many managements are not suffering from The Dunning-Kruger effect. Insurance is a market rife with inefficiencies and, from the outside, it might look easier to be able to make changes.

As we discussed in a previous note, the Gartner Hype Cycle details market expectations for disruptive technologies. Hype and visibility for the new product first rises to a peak of inflated expectations before dropping down when investors are disillusioned with the effect of the technology, until market expectations finally stabilize as the technology matures into a productive niche in the disrupted industry.

The collapse in market expectation for Root and other InsurTech companies that we see now indicates a movement from the second and third stages, potentially to the fourth stage.

This is a positive for InsurTechs as well as the legacy carriers. Irrational competition does not benefit either them or the broader industry.

When many of these carriers came on board with frothy top-line expectations, we were a bit surprised by some of the numbers in their plans. After all, insurance is an industry with low barriers to entry, but once you are in it can very quickly turn into a hedge maze rather like the one at the Overlook Hotel in The Shining.

Many of these InsurTechs are down from their IPO prices, with Lemonade being the only outlier. Examining how these companies were valued using a FinTech model calls for revisiting that thought process itself. Using EV/Revenue, or EV/DPW as a blended valuation measure, likely understated the COGS issue down the road and could in itself be a separate thought piece. New lessons are being learnt on both sides of the aisle, which will likely result in realistic valuations coupled with a slowing down of funds flowing into the sector. You can only throw so much good money after bad money before you say, "I’m out”.

Contending with serious challenges to its growth model, Root’s management team is now faced with a decision on how to proceed, with three starkly different options available. Unfortunately, none of them offer an easy solution; we discuss the pros and cons of each approach below.

Option 1: Consolidate or get acquired? No Nirvana in Carvana

Along with the difficult result, Root announced a relationship with Carvana. Carvana advertises so heavily that it’s likely that you, the reader, have seen an ad for this used car online marketplace. Carvana has benefited from the Covid disruption making money from the run on used-cars pricing, selling loans, and vehicle-servicing contracts. As a result, its stock has seen a meteoric rise of 85% over the past 12 months. With that currency, it was easy to invest in a battered Root.

We don’t see this relationship as a necessary panacea for Root. The discussion of buying insurance at the point of sale has been around for quite some time. For example, Elon Musk’s tweets on auto insurance tend to get everyone riled for a few days before disappearing from news coverage. A bundled insurance product makes sense, but with Root watching its bottom line and its marketing spend, it’s unclear if this partnership will deliver real tangible benefit in the near or even medium term. With less brand recognition, buyers could end up looking elsewhere for their auto insurance needs.

We have mentioned that legacy insurance companies with their balance sheets at multiples of these new companies can afford to sit back in the past. As InsurTechs stumble and figure their way out and the herd thins, the legacy companies have the optionality of acquiring these companies. This will be a likely outcome for many InsurTechs down the road. Root is not that point imminently, although perversely, its challenges could make it more attractive to potential buyers. A potential buyer might feel that at least some of the plans have been battle-tested.

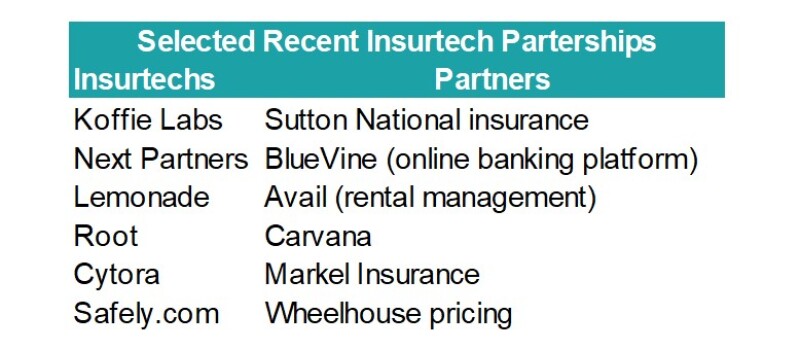

We have already seen an uptick in take-outs and significant partnerships.

This pattern also follows a spate of activity in the FinTech sector, as shown in the exhibit below. So an uptick in consolidation should not be viewed as a surprise.

Option 2: Meander and try to figure it out

In its 1993 report on insurance carriers over time, McKinsey found an interesting outcome. The best performers kept on winning. However, the underperformers struggled to mean revert even when their strategies were revisited several years apart.

With its earnings report, Root cut its guidance which saw the stock sell-off. However, Root is not the only InsurTech to cut its guidance. We have seen other carriers revisit theirs. This is a significant development. Growth companies don’t usually revisit their plans so early out of the gates, and perhaps InsurTechs will scale back their ambitious growth plans. It could also serve as a template for other InsurTechs who are waiting in the wings.

Over time InsurTechs, at least in the mid-term, will fall into this niche of a somewhat viable operation but not necessarily displacing the leaders, as was discussed and anticipated by them in their initial pitches.

The chart below shows an interesting deviation. InsurTechs are recalibrating their plans, and a more balanced outlook on growth might serve them well, although this creates a vicious cycle. The high stock multiple was contingent on growth plans. Root and others will end up having to accept a more realistic valuation. This slowdown could also hinder their ability to raise additional capital, which could end up creating a vicious circle of slowing down growth!

The table below shows the shift in guidance. We would not be surprised to see Root and other InsurTechs continue to revisit their guidance/expectations down the road.

Option 3: Fail into oblivion

Last week Root’s results, guidance shift, stock market reaction, and analyst price target revisions brought back the usual question. Are we heading into a death spiral for these companies? Will they be able to come back like an Apple or a Best Buy? Although one should not forget that for every Apple and Best Buy there is Blackberry and a Circuit City.

And with poor retention numbers shown below, it’s not that these companies are making much headway in building a stable book of business.

The vast class of InsurTechs promised investors the ability of AI and ML to be better able to slice and dice the book. However, the gap between legacy and these companies remains stubbornly wide.

In the recent earnings cycle, legacy and InsurTech writers noted that the recent uptick in loss cost trends was pressuring results. In our piece on Lemonade, we noted this unexpected new normal could be the start of a new trendline.

The vast class of InsurTechs promised investors the ability of AI and ML to be better able to slice and dice the book. However, the gap between legacy and these companies remains stubbornly wide.

In the recent earnings cycle, legacy and InsurTech writers noted that the recent uptick in loss cost trends was pressuring results. In our piece on Lemonade, we noted this unexpected new normal could be the start of a new trendline.

There has also been some debate about the capital adequacy of Root and other players. As of Q2:2021 Root’s shareholders’ equity was $762mn apart from Carvana’s investment of $126mn. If loss-cost trends continue to worsen materially, as discussed in our personal auto piece, Root will continue to have to revisit its growth plan. This could increasingly put it on a path to irrelevance and an eventual take-out at run-off valuations.

We view this as a low likelihood at this juncture. Further, personal auto is a short-tailed line, and any company can take drastic rate action to steady the ship. This could result in a big hit to the top line, but the capital would be protected until the company recalibrates its strategy.

Many insurance companies have traded and continue to trade at a significant discount to the peer group and can linger around for years if not decades. So yes, unlike the legacy companies such as Allstate and Progressive, the InsurTech cohort is watching a steady erosion in their capital.

All three options mentioned above promise a difficult path forward for Root, and InsurTechs as a whole. In Root’s case specifically, it could be a tough clawing back if broader loss-cost trends continue to worsen. In any event, we are at a pivotal moment in the InsurTech space, where this quarter's earnings results and stock reaction will have far-reaching implications for the insurance industry.