Speaking of parties, one of the biggest is going on right now in the property-catastrophe reinsurance space. A combination of events including Hurricane Ian, the recent uptick in large losses, rate inadequacy, and the third-party capital freeze are expected to result in a meaningful uptick in rates.

Many companies who have sat on the sidelines for years have recently expressed an interest in examining opportunities at the upcoming reinsurance renewal cycle. Axis, on the other hand, is on its way to transition out of volatile classes including a planned exit from the property reinsurance business. Talk about timing!

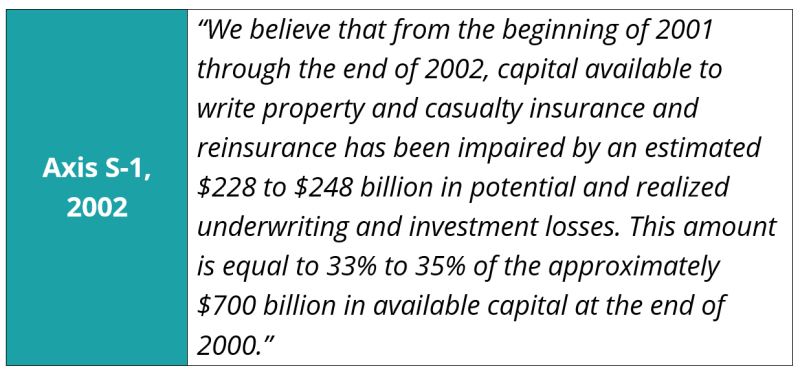

On the topic of timing, it makes sense to revisit the formation of Axis. Axis was one of several companies formed after the 9/11 tragedy to capitalize on the market hardening.

Axis’s S-1 at that time also talked about the market exits of Gerling, Scor, Axa, and Overseas Partners going on at that time, as well as ratings action on one-third of the largest 150 reinsurers. But like many other companies formed at that time, Axis ended up at the same great fork in the road. What to do with the franchise when rates are no longer attractive in your core classes?

In most cases, we have seen one of four outcomes: (1) sticking to your knitting, and growing or shrinking and returning capital when not needed; (2) moving into unrelated lines and trying to learn the book after the fact; (3) trying to balance the insurance/reinsurance mix and hoping to time the spigots well; or (4) seeing the writing on the wall and selling the franchise.

Albert Benchimol, Axis’s current CEO, is in a tough place. The chart below shows Axis’s price to tangible book (ex AOCI) multiples over time compared to a mix of reinsurance/insurance/specialty-centric carriers.

If stock price is a report card of how the returns have been viewed by the market, getting lumped in next to the ever-struggling Argo is cause for concern.

Axis has seen a meaningful level of change since its inception, including a tumultuous management transition a decade ago.

Our note will cover this later in detail, but this amount of evolution in the franchise, including key leadership changes, leaves the franchise in “fixing-it” mode vs. being able to step back and evaluate it over a multi-decadal period. Axis's latest pivot seeks to lean into the specialty insurance side of the equation.

In this move, the company has banked heavily on Vince Tizzio who was announced as CEO for specialty insurance and reinsurance at Axis following a reshuffle at the top.

Tizzio spent time at Navigators and The Hartford, both companies we covered as equity analysts in the past. The Hartford’s takeout of Navigators and its subsequent challenges do give Tizzio a “what not to do” playbook.

Taking a step back, Tizzio leads Axis’s insurance franchise at a time when the industry is facing a unique set of challenges. On the plus side, insurance pricing continues to be stable, and inflation adds to the revenues, while on the flip side, the loss cost inflation and social inflation still remain big unknowns.

Benchimol and Tizzio have to navigate this new normal. With the stock trading at or around book value for a while, there is less room for trial and error and any noise in the numbers from this pivot.

Beyond change, Axis has continued to address the volatility in its books. As our note shows, the reduction of its PML precipitously intersects with an anticipated industry pricing uptick of multiples of historic asks.

We recognize that it’s easy to be armchair critics like us. That said, not closing the door fully would have put Axis in a position to be extremely selective on market opportunities. This will not be the case anymore at January 1.

Currently, Axis sits on the lower end of value creation measured by book value growth over time which is reflected in its anemic stock multiple. Had the returns been similar to franchises such as RenaissanceRe, the stock would have been higher by 40% to 60% when considering the peer group multiple regression.

The note below looks at these three factors in detail.

Firstly, the company has seen meaningful change in its short history

Axis and several others in the so-called “Class of 2001” were formed after the 9/11 tragedy to benefit from a capital squeeze. Since that time, both reinsurance and insurance markets are in a materially different place. In fact, market conditions have changed so much that most of the standalone franchises are no longer independent.

From the Class of 2001, only Arch Capital (successfully pivoting to mortgage insurance) and Axis still exist as standalone entities. Allied World, Endurance, and Montpelier Re all were subsumed by larger franchises. We covered the changing landscape in our aptly titled note “Where have all the reinsurers gone”?

The table below sourced from Axis’s news releases shows the timeline of events, and readers will likely notice several changes over the years.

Apart from the Class of 2001, the markets also witnessed the Class of 2005 Bermuda/hybrids formation which included names such as Validus, Ariel, Flagstone and Harbor Point. These names have been subsumed into other companies as well.

Part of the industry consolidation (Flagstone, Transatlantic) took place when Axis was seeing a leadership succession from John Charman to Benchimol (in 2012). Another big wave of consolidation (Allied World, Endurance, Montpelier, Catlin, Platinum) came around the time Axis was in the middle of its own attempts to merge with PartnerRe.

This level of industry consolidation has left a smaller list of companies potentially looking to expand their franchise via an Axis takeout. Therefore, Axis’s only remaining course of action is to make this iteration of their business work.

Longer term, this could translate into an attractive franchise for potential buyers as capital deployment opportunities for the industry wane.

Secondly, exiting the property-cat market will be a one-way door decision

The graph below shows combined ratios on a quarterly basis going back to 2004. Note the shift over time in both classes and the more pronounced shift in the reinsurance segment over time.

Splitting the chart below in half reveals that reinsurance's combined ratio was below 100% (profitable) 82% of the time vs 70% in the second half. Insurance's CR was below 100% for 84% in the first half vs 73% in the second.

With the return in volatile classes diminishing over time, investor sentiment has turned. Additionally, the impact of volatile results is more visible for companies with a smaller marker capitalization, compared to some of the biggest reinsurers of the world. This has resulted in Axis continuing to cut back these classes over time.

The chart below plots US rate-on-line (ROL) data vs Axis’s south-east hurricane one-in-100 probable maximum loss (PML) shift. Recall that ROL is premium charged divided by reinsurance limit and hence this index is a proxy for market conditions. The one-in 100-year PML means that the loss amount has a 1% probability of being equaled or exceeded in any given year.

Had Axis moderated its growth earlier in the cycle and reined in its PML and the subsequent volatility, it could have had a chance to play in this rate environment. That opportunity is going to be lost as the company continues with its current strategic shift.

The chart below shows what’s going on behind the scenes at Axis. Axis believes that it will continue executing on the improvement in its underlying loss ratio in its insurance segment (low 50s). Coupled with cat loss moderation, this would enable it to achieve an overall underlying loss ratio in the 50s.

This coupled with a low 30s expense ratio will put the company in the sub-90s combined ratio on an underlying basis – an aggressive target to maintain year-after-year if industry loss cost trends worsen.

Thirdly, a pivot addresses volatility short-term but value creation remains the true litmus test

The chart below shows underwriting income by segment over time against total investment income. The company does not apportion investment income in its disclosure, but note that long-tail classes in insurance would have a greater impact than short-tail classes with shorter duration.

The chart below also illustrates reinsurance’s meaningful contribution in the middle part of the last decade before slowly petering out.

How does this all add up? Firstly, although results can look good over a shorter period of time, value creation over time is the only true proxy for getting it right over industry cycles. Secondly, a close correlation does exist between longer-term value creators and their stock multiples.

What this means is that companies with the highest value creation typically cluster, having a higher price to book multiple.

The chart below stratifies carriers based on their price to tangible book value (ex AOCI) and their 15-year value creation CAGR, with those in the top right representing better metrics. As can be seen, Axis’s challenges have weighed on its value creation and consequently clubbed its valuation leaving it far behind the rest of the pack.

As a hypothetical exercise, if Axis’s value creation CAGR was in the 10% range, factoring in the regression equation shown below, it would have resulted in a mathematical stock price of $87/share! A more realistic multiple closer to RenRe would still equate to a 40% upside or $76/share vs. current price of $54.67/share.

Translation: The company will have to exhibit value creation over a period of time to enable it to close its valuation gap compared to its peers.

In summary, the pivot away from volatile classes has assuaged investors shorter-term. On the insurance side, the industry faces mixed signals and an uncertain economic climate.

Getting the loss cost inflation side right is paramount for Axis as we flatten out of a peak commercial pricing environment.

Only consistent insurance results will translate into consistent value creation, something we have seen at franchises such as Arch, RenRe or WR Berkley. If Axis doesn’t get it right, there might not be many invites left for other parties.