The strong bottom line performance was due to a higher organic growth and lasting cost efficiencies associated with the pandemic. The broker reported a strong 9% organic growth in its commercial risk segment, the highest in more than 17 years. Most other segments expanded by mid-single-digits except data & analytics that was down 2% following three back-to-back quarters of 7% to 8% contractions.

Aon expectedly grew more bullish on the prospective growth as it upgraded its full year 2021 organic growth guidance to “mid-single-digit or higher,” following similar actions from Marsh McLennan and AJ Gallagher.

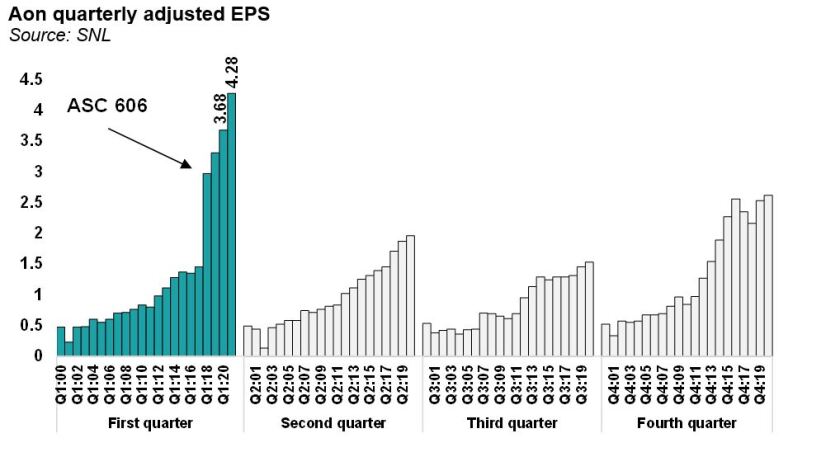

Lastly, in line with Marsh McLennan, Aon highlighted long term implications on client interactions from the pandemic.

As we discussed in the beginning of the year, the economy-sensitive brokerage industry may be entering a highly favorable environment with multiple tailwinds blowing in the right direction at the same time. These include high rates, exposure growth, economic growth and other more fundamental industry-specific forces that we highlight in our quarterly broker wraps. These trends are likely to persist and even intensify over 2021, which may result in the best year for intermediaries’ organic revenues since 2001-2003 hard market.

On the proposed Willis merger, management provided fewer details than the industry followers might have hoped for. Perhaps the only material update was the public acknowledgment of the remedies being offered to the regulators.

Otherwise, the broker provided no updates on the $800mn cost synergies and combined entity organic growth target (“mid-single-digit or greater" prior to dropping it in Q1:20 in response to the pandemic). These items will remain highly watched in the coming months/quarters. The focus appears to be shifting from antitrust issues to potential value destruction from divestitures and potential talent flight.

A potential of value migration to AJ Gallagher has also become a hotly discussed topic if it gets some large and highly profitable assets out of this transaction. These could potentially include Willis Re and Western European broking assets, as reported by our colleagues on the Inside P&C news team and by Insurance Insider. We may still end up having Big-3 brokers instead of expected Big-2 when the transaction closes, and dust settles.

Elsewhere, Aon echoed the earlier comment from Willis on its expectation to close the transaction by the initially announced deadline of June 30. However European Commission (EC) announced earlier that it is extending the Phase II review deadline till July 27 with a potential from Australian regulators to follow suit.

This may serve a signal that the merging parties are close to receiving the approvals in key jurisdictions.

In summary, Aon’s report served as a confirmation of the trends emerged during this brokerage earnings season. With all public brokers hitting mid-single-digit organic growth at least one quarter ahead of expectations, the bar is set high now for the balance of the year. With the industry tailwinds persisting, macro fundamentals improving and the comparison growing favorable, are we set to see a streak of double-digit organic growth figures on brokers in the coming quarters?